If your insurance company has asked for a four point inspection — or if you’re buying an older home in Central Florida and your agent mentioned you’ll need one — you’re not alone in wondering exactly what it is, what it looks at, and whether it’s the same thing as a regular home inspection. It isn’t, and understanding the difference will save you time, money, and a few phone calls.

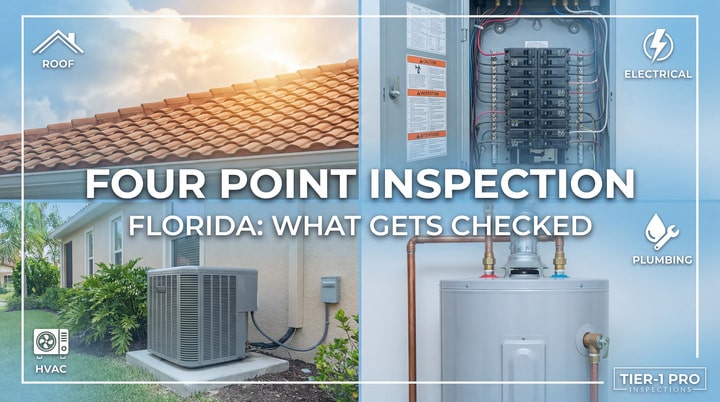

A four point inspection is a focused insurance review of the four major systems in a home: the roof, the electrical system, the plumbing system, and the HVAC. That’s it. It doesn’t cover the full scope of a standard home inspection — no attic insulation, no window operation checks, no door hardware — because its purpose isn’t to evaluate the overall condition of the home for a buyer. Its purpose is to give an insurance underwriter enough information to decide whether they’re willing to insure the property and at what terms.

Florida insurers began requiring these inspections largely because of the state’s catastrophic storm exposure and the financial losses carriers absorbed during the major hurricane seasons of the 2000s. After that period, many companies tightened their underwriting standards significantly, and the four point inspection became a standard gate for older homes. Today, most Florida insurance carriers require one for homes that are 10 years old or older, though the threshold varies by company. Some carriers require them on homes as new as five years old. If you’re refinancing, renewing a policy with a new carrier, or purchasing a home built before the mid-2010s, there’s a reasonable chance you’ll need one.

What Inspectors Actually Evaluate

The roof section of a four point inspection covers the material type, the estimated age, the overall condition, and whether there are visible signs of damage, active leaks, or previous repairs that may have introduced new vulnerabilities. Insurers pay close attention to roof age in Florida because the state’s UV exposure, heat cycling, and storm season put roofs under stress that accelerates wear faster than in most other parts of the country. An asphalt shingle roof that might last 25–30 years in a northern climate may reach the end of its insurable life in 15–20 years here. Some carriers will decline to write a new policy if the roof is beyond a certain age, regardless of its current condition. Others will insure an older roof but exclude wind and hail coverage or add a premium surcharge. What the inspector documents in this section directly shapes that decision.

The electrical portion is where four point inspections generate the most friction for homeowners. The inspector evaluates the panel brand, the type of wiring, the age of the system, and the condition of visible components. Certain panel brands — Federal Pacific Electric Stab-Lok, Zinsco, and Pushmatic among them — are known to have documented defect histories, and Florida insurers treat them as high-risk. If one of these panels is present, the insurer may require replacement before binding coverage or may decline to write the policy at all. The inspector also looks for aluminum branch wiring, which was common in homes built in the 1960s and early 1970s and carries a higher fire risk than copper wiring when improperly maintained or terminated. Double-tapped breakers, open knockouts, and visible signs of amateur electrical work are also noted.

The plumbing section focuses on the supply and drain materials throughout the home. The inspector identifies what the pipes are made of and notes the approximate age and visible condition. Common materials include:

- Copper

- CPVC

- PVC

- Galvanized steel

- Polybutylene

- Cast iron

Polybutylene is the material that draws the most attention here. It was used widely in Florida homes from the late 1970s through the mid-1990s and has a well-established history of failing at fittings and connections without warning. Many insurers will not write a policy on a home with active polybutylene supply lines. Galvanized steel, while not as acutely problematic, corrodes from the inside out over time and is noted as a concern in older homes. Cast iron drain lines, common in pre-1975 construction, are also flagged due to their corrosion-related deterioration, particularly in Central Florida’s soil conditions.

The HVAC section covers the heating and cooling systems — the equipment type, the approximate age, and the visible condition of the units. In Florida, the practical concern here is almost entirely focused on air conditioning, since dedicated heating systems are minimal or absent in most homes. The inspector notes the age of the equipment (often decoded from the serial number) and whether it appears functional and properly maintained. Insurers are less likely to deny coverage based on HVAC condition alone compared to the other three systems, but a very old or visibly deteriorated system will be documented and may factor into underwriting decisions, particularly if it creates a secondary risk like water damage from a failing condensate drain.

When You Need One and Who Orders It

The most common trigger for a four point inspection is a change in homeowner’s insurance — either purchasing a new policy when buying a home, switching carriers at renewal, or receiving a notice from your existing insurer requiring an updated inspection. Insurance companies typically set their own requirements for how frequently they need a new four point report, though a common standard is every five years. Some carriers will accept a report that was completed in connection with a recent home purchase if it’s current enough.

If you’re buying a home in Central Florida and the property is more than 10 years old, it’s worth having the four point inspection done at the same time as your pre-purchase home inspection. Doing them together saves you the cost of a second mobilization and gives you the insurance documentation you need before you go to bind your homeowner’s policy. Discovering a problematic panel brand or active polybutylene plumbing for the first time at the insurance stage — after you’ve already closed — puts you in a much weaker position than knowing about it before the transaction is final.

Sellers who are preparing to list an older home may also find it useful to order a four point inspection in advance as part of a pre-listing strategy. If there are issues a future buyer’s insurer will flag, knowing about them early gives the seller the option to address them on their own timeline rather than under the pressure of a pending closing.

What the Report Looks Like

A four point inspection produces a standardized report — most Florida inspectors use the Citizens Insurance four point form, which is widely accepted across carriers because Citizens is the state’s insurer of last resort and its form has become the de facto industry standard. The report includes photographs of each of the four systems, the inspector’s findings, and fields that document materials, ages, and conditions. The completed report goes directly to your insurance agent or carrier, who uses it to determine eligibility and pricing.

The inspection itself typically takes between 30 minutes and an hour for a standard-sized home, and the report is usually delivered the same day.

People Also Ask

Is a four point inspection the same as a home inspection?

No. A four point inspection is a limited insurance review covering only the roof, electrical, plumbing, and HVAC systems. A standard home inspection covers the full condition of the property — structure, foundation, exterior, interior, insulation, windows, doors, and all mechanical systems in much greater detail. A four point inspection tells an insurer what it needs to know. A home inspection tells a buyer what they need to know. They serve different purposes and neither one replaces the other.

How much does a four point inspection cost in Florida?

Pricing varies by company and region, but most Central Florida inspectors charge between $75 and $150 for a standalone four point inspection. When bundled with a full home inspection, the add-on cost is typically lower. Bundling is the most cost-effective approach for buyers and is worth asking about when scheduling.

What happens if my home fails a four point inspection?

There’s no official pass/fail — the inspection produces a factual report, and the insurance carrier makes its own underwriting decision based on what’s documented. If an issue is found (a problematic panel brand, polybutylene plumbing, a very old roof), the carrier may decline coverage, require repairs before binding, or offer coverage with exclusions. In most cases, addressing the specific issue and providing documentation of the repair resolves the situation.

How old does a home have to be to require a four point inspection in Florida?

Most carriers require it for homes 10 years old or older, though this threshold varies. Some companies apply it to homes as young as five years old, and some require it regardless of age if the home has had certain types of prior claims. Your insurance agent will know the specific requirements for the carriers they work with.

Is a four point inspection required by law in Florida?

No. It’s required by insurance companies, not by state law. The requirement is a private underwriting decision made by individual carriers. However, since you cannot legally own a mortgaged home without homeowner’s insurance, and since most Florida carriers require the inspection for older homes, it functions as a practical requirement for the vast majority of buyers and homeowners in the state.

How long is a four point inspection valid in Florida?

Most carriers accept a four point inspection for three to five years, but this varies by company. Some carriers will continue to honor an older report if no significant changes have been made to the covered systems. Ask your agent how long the report will remain valid with your specific carrier before scheduling.

“`